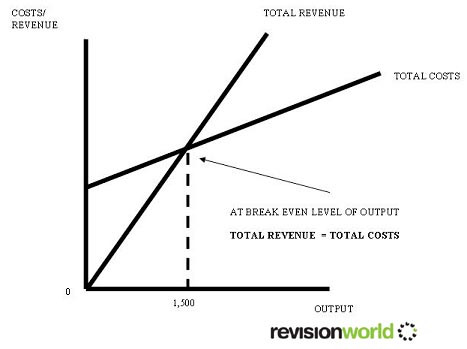

Break even is the point of production where are firms revenue is equal to the total costs of production

Margin of safety – the difference between the firms current level of output and break even output

Break even = Fixed costs / contribution per unit

Break even analysis can help managers to plan and in their operations. In addition it can help:

- Analyse the impact of a change in the environment on the business

- Decide whether or not to accept an order for products at a different price from normal

Break even analysis can use a number of methods:

- Contribution method

- Break even chart

- Break even graph

Break-even diagram

Image

Uses of break-even analysis

- Allows to decide if a business venture is financially viable

- Looks at what will happen if level of production changes

- To support an application for an external source of finance e.g. loan or mortgage application

Changes in the business environment and break even

- If Variable Costs (VC) rise in value then break even output increases

- If VC fall in value break even output decreases

- If Fixed Costs (FC) rise break even output increases

- If FC fall break even output falls

- If selling price increases break even output decreases

- If selling price decreases break even output increases